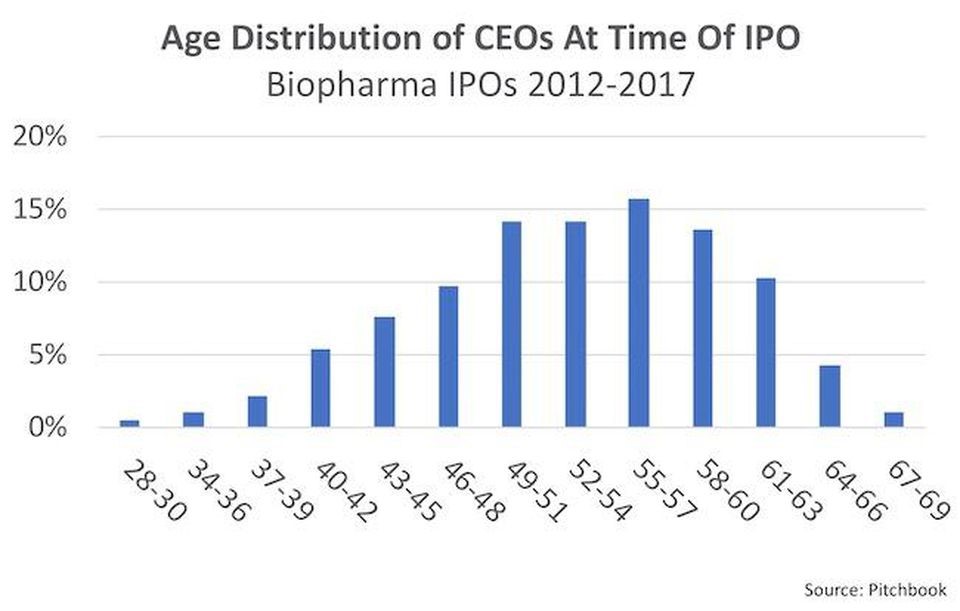

Without question, ageism exists in biotech. Recently, a feature in Forbes (Gray Hair in the C-Suite: Experience, Age and IPOs in Biotech) highlighted that the median age of biopharma CEOs at IPO was 54 years, and 75 percent were 48 or older. I’ve experienced ageism. At 37 years, I am more than 15 years younger than the median biotech CEO. The average age of first-time CEOs at IPO is 51. While this should be surprising to no one, it does beg the question of whether age has bearing on one’s ability to lead a company to a successful outcome. I raise the question here because there are strong parallels to academia. University labs are for most intents and purposes ‘small companies’ with equivalent budgets and comparable organizational structures. The principal investigator of an academic lab holds an equivalent position to the CEO of a company, and challenges securing ones first “faculty” position, startup and ongoing funding, and strategic partnerships are identical to those faced in business, particularly as they relate to age and experience.

Does age matter?

To be clear, I am not disputing that experience matters – the questions I am interested in deconstructing are ‘is age a proxy for experience?’, ‘is experience a proxy for performance?’, ‘how much do either age or experience matter in leading a biotech company?’ and ‘in what contexts do they impact outcome?’. In Gray Hair in the C-Suite: Experience, Age and IPOs in Biotech Bruce Booth extends the work of Katrine Bosley to elaborate on the question of whether age matters by introducing more data into the conversation.

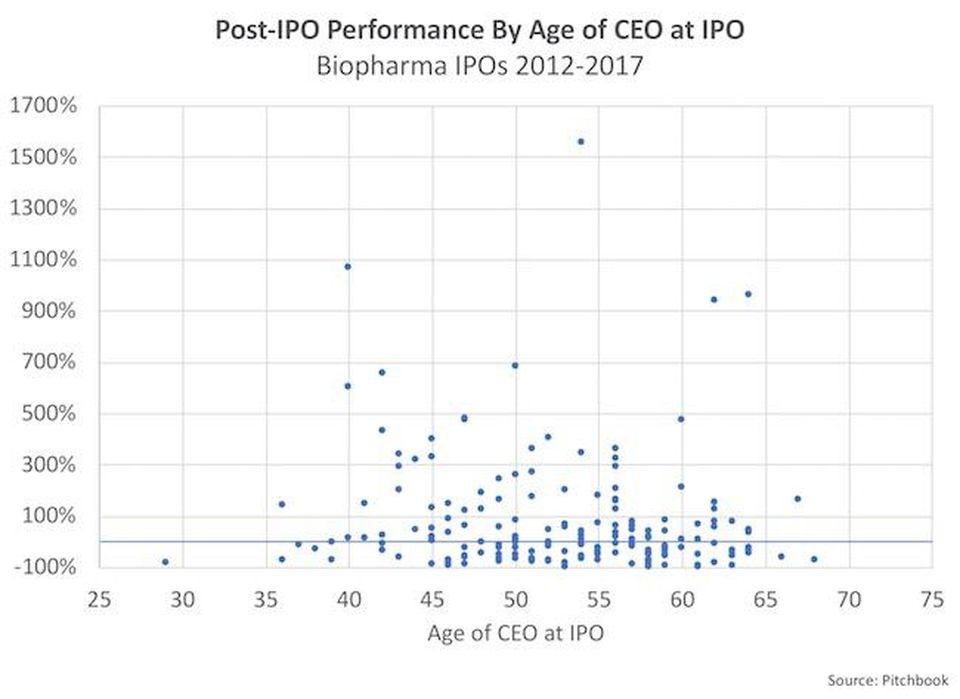

Among the data shared is evidence that post-IPO stock performance has no correlation with CEO age at IPO in biopharma, and performance doesn’t change relative to the founding status of the CEO. Similar studies have found no statistically significant relationship between long-run aftermarket performance and director experience at the time of an IPO, and no material patterns have been observed between CEO age and subsequent abnormal shareholder return performance. Where then is age relevant?

Context matters

Mr. Booth appropriately notes that if the median time to IPO is six to seven years, the typical founding CEO must have been in their mid-40s when they started the company. Founding CEOs in their mid-40s at IPO would presumably have been in their mid-to-late 30s. Non-founding CEOs are generally older. This is comparable to the median age of first assistant professor position in academia, which is typically related to acquiring one’s first RO1 grant from the National Institutes of Health in the United States (an equivalent of seed funding in biotech, see Future of fundamental discovery in U.S. biomedical research). Statistics are comparable for Canada, and reinforce a trend of increasing age of full-time faculty (Figure 5, below). Since academic labs are always founded around an assistant professor, who is never replaced as the director of the lab, founder-CEOs are the closest comparator.

While these data reinforce the observation that investors want to back directors who are older, it doesn’t address the fundamental question of whether age is a proxy for success.

The common narrative that is often advanced (without data) is that younger CEOs, like junior faculty, lack experience in leadership that introduces management risk to an already risky venture. More experienced directors are therefore “likely to be better at R&D risk identification/mitigation strategies and appropriate resource allocation; further, they will typically bring value-added broader networks, built over their careers, into pharma decision-makers and the capital markets to leverage for downstream liquidity” (Gray Hair in the C-Suite: Experience, Age and IPOs in Biotech).

My next post will explore a different narrative.

Featured Jobs

- History - Lecturer or Assistant Professor (per course instructors)Huron University

- Health Sciences - (2) Postdoctoral Research Fellowships, 2-Year Term (Rare Dementia Support Canada)Nipissing University

- Physical Education - Probationary Tenure-Track PositionBrandon University

- Law - Assistant or Associate Professor (Law & Public Policy)Queen's University

- Veterinary Medicine - Lecturer, Term (Large Animal Internal Medicine)University of Saskatchewan

More from Opinion

-

Feeling disillusioned? The Pope is on your side

Pope Leo XIV’s encyclical on AI has much to say about the culture of profit, technocracy and competition pervading today’s universities.

-

From research to impact: How graduates transform society

A Université Laval study shows that most research-trained graduates contribute to innovation and act as catalysts for societal change.

-

The race to reimagine higher education

How Canadian universities can lead the AI transformation.

-

Science must become a pillar of Canadian foreign policy

With technological developments reshaping global governance, science cannot remain isolated from international relations.

More from Lab

-

Building a lab: 6 months of triumphs and trials

As head of a lab, you're the one-man band responsible for everything from marketing to finance to product development.

-

A call for widespread adoption of universal MTAs

The current process for material transfer agreements involves way too much paperwork and puts unnecessary stress on both researchers and technology transfer offices.

-

The purpose of branding in science

Branding is the exercise of summarizing an organization’s culture to attract a particular type of employee, collaborator or funder.

-

Incentive structures are needed to ensure scientific progress

We must identify and resolve the gaps in our current scientific training, and revisit and refine the incentive structures we’ve created around our scientists.

More from The Black Hole

-

How to start a company from scratch

Establishing and leading a startup is hard, but it is also an opportunity to do something creative, fun and unique.

-

Yes to more evaluation, but a bigger yes to more action

A recent report on research culture shows that evaluation is key, but stops short of practical solutions to core problems.

-

The art of grant writing: write, rewrite and write again

And don't forget the detailed budgeting and a looming submission deadline.

-

Breaking EDI barriers in science

Clear metrics are needed to evaluate the success of initiatives to remove inequities in the research enterprise.

Post a comment

University Affairs moderates all comments according to the following guidelines. If approved, comments generally appear within one business day. We may republish particularly insightful remarks in our print edition or elsewhere.